May 13, 2026

Parent PLUS Loan Changes for 2026: What Families Need to Know

By Peter Young, Founder of My School List

The One Big Beautiful Bill Act caps parent borrowing starting July 1, 2026. Here is what it means in plain English.

During my twenty-three years in education leadership as an elementary and middle school principal, I learned that the families who do best are usually not the ones with the biggest budget. They are the ones who see the blindspots early enough to make a plan. That is exactly why I want to get this in front of you now.

Right now, a massive shift is coming for parents of high schoolers. If you have a junior or a senior in high school, you need to put down your coffee and look at the calendar.

On July 1, 2026, the federal government is dropping a hammer on the way families pay for college. For decades, the Parent PLUS loan program was essentially an open faucet. If your child got into an expensive school, you could borrow the full cost of attendance. Those days are ending.

Public Law No. 119-21, also known as the One Big Beautiful Bill Act or OBBBA, is about to change your financial life (Department of Education). Whether you are a parent in Atlanta, Bethesda, Minneapolis, or Phoenix, the rules of the game are shifting mid-stream.

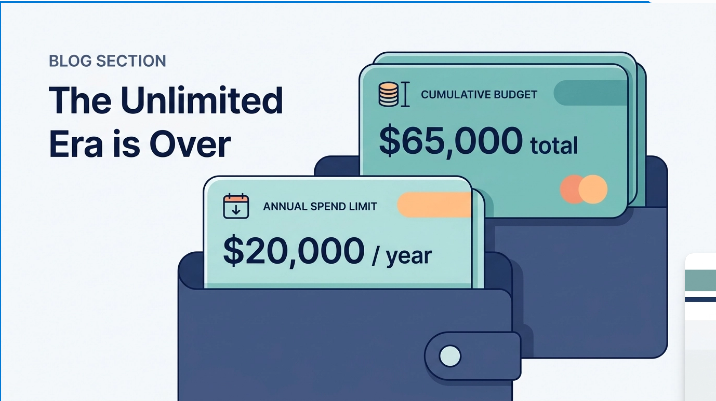

The "Unlimited" Era is Over

For years, Parent PLUS loans were the fallback plan for families who didn't have $80,000 a year sitting in a 529 account. You could borrow up to the total cost of attendance minus other aid. There was no aggregate limit.

Starting July 1, 2026, the OBBBA introduces two major caps that will change your college search strategy. First, there is now an annual cap of $20,000 per student per academic year (NASFAA). That limit is per student, not per parent. If two parents borrow for one child, they still share the same $20,000 total for that student. If your child is heading to a school with a $60,000 gap after scholarships, you can no longer bridge that entire gap with federal parent loans.

Second, there is a new lifetime borrowing limit of $65,000 per student (Public Law No. 119-21). Again, that cap is tied to the student, not to each individual parent. This is the part that catches most families off guard. If you borrow the maximum $20,000 for the first three years, you will hit your lifetime limit before your child even starts their senior year.

The Math Trap: $20k x 4 is not $65k

Let's look at the math because it is the most important part of this entire policy. If you are planning to use Parent PLUS loans to cover a significant portion of a four-year degree, you are walking into a trap.

If you borrow $20,000 for freshman year, $20,000 for sophomore year, and $20,000 for junior year, you have used $60,000 of your $65,000 lifetime limit. When senior year arrives, you only have $5,000 left in the federal tank.

For families looking at top-tier private universities or out-of-state flagships, this $65,000 lifetime limit is a very low ceiling. You cannot simply "loan your way" through an expensive degree anymore.

The Repayment Sting

It isn't just about how much you can borrow. It is also about how you have to pay it back. Previously, parents had access to various income-driven repayment plans that could make the monthly burden manageable based on their earnings.

For loans originated after July 1, 2026, those options are vanishing. New borrowers will be funneled into a tiered standard repayment plan that lasts between 10 and 25 years (Department of Education).

Perhaps the most painful change is what happens to Public Service Loan Forgiveness, or PSLF. Many parents work for federal agencies, non-profits, or local governments and have been counting on PSLF as part of their long-term plan. PSLF is not gone, but for most parents who borrow under the new rules, the path is gone in any practical sense. New Parent PLUS loans after July 1, 2026 are limited to the new Standard Repayment Plan, and only the 10-year version of that plan qualifies for PSLF, which will not apply to most borrowers given the new loan balances (Public Law No. 119-21; Department of Education). For federal workers, non-profit employees, and other public-service borrowers, this is a meaningful change.

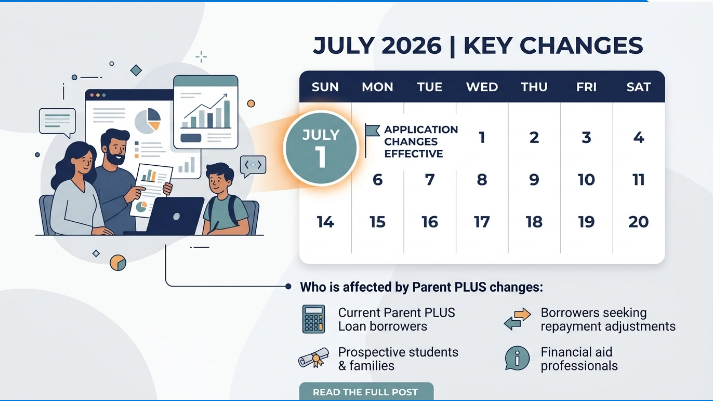

Who is affected: Class of 2026 vs. 2027

If you have a senior in the Class of 2026 who is heading to college this August, you have a small window of protection. The law includes a legacy rule for parents who borrow before the July 1 deadline.

If you take out your first Parent PLUS loan for a student before July 1, 2026, you qualify for a legacy provision that allows you to continue borrowing under the previous rules for three years or until your student completes their current program, whichever comes first. The student also has to remain continuously enrolled in the same program at the same school (NASFAA; Public Law No. 119-21). In practical terms: most Class of 2026 families starting freshman year this August will be covered for years 1 through 3, then hit the new caps for year 4. If your student transfers schools or takes a leave of absence, legacy status ends and the new caps apply immediately.

However, if you have a junior in the Class of 2027, you are heading straight into the new world. There is no grandfathering for you. Every dollar you borrow will be subject to the $20,000 annual and $65,000 lifetime caps.

What this looks like in practice

Here is one concrete scenario that shows how the new caps change the math.

A family is considering a private college with a $70,000 annual cost of attendance. Their estimated Student Aid Index, or SAI, is $25,000, which puts them in the middle-income range. After grants and scholarships, the school's net price comes in around $50,000 a year.

Under the old Parent PLUS rules, the parent could borrow up to the full cost of attendance minus other aid. That meant borrowing $40,000 or more a year was structurally possible, with no aggregate lifetime cap. Four years of that kind of borrowing was rough, but doable on paper.

Under the new OBBBA rules, the same family runs into two walls.

First, the annual cap. The parent can borrow no more than $20,000 a year. If the net price is $50,000 and the family contributes their $25,000 SAI, the gap is still $25,000 a year. The $20,000 cap covers most but not all of that gap. There is still a $5,000 annual shortfall to find somewhere else.

Second, the lifetime cap. Even if the family is comfortable borrowing the full $20,000 every year, four years of that adds up to $80,000. That exceeds the $65,000 lifetime cap by $15,000. So in practice, the family can borrow $20,000 a year for the first three years and $5,000 in year four, and that is it.

The new math forces a different family conversation. Options include drawing more from savings, taking out private (non-federal) loans for the gap, hunting for additional merit aid or outside scholarships, or revisiting the school choice itself. None of those are bad outcomes, but they are different decisions than the family would have made under the old rules.

To run this math on a specific school, use our free Affordability Estimator. The tool shows your estimated net price plus your Parent PLUS gap under the new $20,000 cap, for any school in our database.

Frequently asked questions

What is the OBBBA?

The One Big Beautiful Bill Act is the federal law (Public Law No. 119-21) that includes the new Parent PLUS borrowing caps. It was enacted in 2025 and takes effect for federal student loans originated on or after July 1, 2026. The law also changes graduate student lending and federal repayment plans.

When do the new Parent PLUS rules take effect?

The new caps apply to any Parent PLUS loan originated on or after July 1, 2026. Loans originated before that date generally follow the old rules under a legacy provision, with some conditions tied to continuous enrollment in the same program.

How much can parents borrow under the new rules?

Parents are limited to $20,000 per student per academic year in Parent PLUS loans. That cap is per student, not per parent. If two parents borrow for the same child, they share the same $20,000 total for that student.

What is the lifetime borrowing limit?

There is a new lifetime cap of $65,000 per student in total Parent PLUS borrowing. If you borrow the full $20,000 in each of the first three years, you will hit the lifetime cap before your child's senior year. The cap is tied to the student, not to the parent.

Does this affect students currently in college?

It affects new loans, not existing ones. Parents who already have Parent PLUS loans from before July 1, 2026 keep their original terms on those loans. A legacy provision also lets parents who took their first Parent PLUS loan for a student before July 1, 2026 keep borrowing under the old rules for that student for up to three more years or through the end of the student's current program, whichever comes first, as long as the student stays continuously enrolled in the same program at the same school.

What about graduate students?

Graduate students face their own changes under OBBBA. Federal Grad PLUS loans are being eliminated for new borrowers on or after July 1, 2026. Graduate borrowing will be limited to the underlying Direct Unsubsidized Loan limits, which are far lower than what graduate students could previously borrow.

Are Pell Grants affected by these changes?

The Parent PLUS caps do not directly change Pell Grant eligibility or award amounts. Pell continues to be determined by the federal Student Aid Index from the FAFSA. OBBBA does include some adjustments to Pell, but the loan caps and the Pell program are separate questions and should be tracked separately.

What about the FAFSA changes parents are hearing about? Are those OBBBA too?

No. FAFSA Simplification is a different law from 2020 (the FAFSA Simplification Act) that has been rolling out over multiple years. That is the change that replaced the Expected Family Contribution with the Student Aid Index and adjusted how having siblings in college affects federal aid calculations. OBBBA is a separate 2025 law that focuses on loan caps and repayment plans. The two laws often get conflated in news coverage, but they are different.

Does this affect existing Parent PLUS loans?

No. Loans that were already originated before July 1, 2026 keep their original terms. However, if you have existing Parent PLUS loans and want to preserve access to income-driven repayment, the timing matters. You will need to consolidate into a Direct Consolidation Loan, and that consolidation must be disbursed by June 30, 2026. This is a disbursement deadline, not an application deadline. Processing typically takes 30 to 90 days, so the Department of Education recommends submitting consolidation applications by April 1, 2026 to leave enough margin. There is also a second deadline: after consolidating, borrowers need to enroll in Income-Based Repayment by July 1, 2028 to keep long-term IDR access. A legacy provision also lets parents who took their first Parent PLUS loan for a student before July 1, 2026 keep borrowing under the old rules for that student for up to three more years, as long as the student stays continuously enrolled in the same program at the same school.

What families can do right now

This news feels heavy, but I don't want you to panic. I want you to plan. As a former principal, I know that information is the best cure for anxiety. Here are five concrete actions you should take in the next 60 days.

1. If you already have Parent PLUS loans, act on consolidation now.

For parents with existing Parent PLUS loans, preserving access to income-driven repayment may depend on consolidating into a Direct Consolidation Loan and having that consolidation disbursed by June 30, 2026, not just submitted by then (Department of Education; NASFAA). In practical terms, the recommended application window has already passed. Borrowers who still need to consolidate to preserve income-driven repayment access should apply immediately, but should know that the Department of Education's consolidation processing typically takes up to three months, and any consolidation that does not disburse by June 30, 2026 will permanently lose access to income-driven plans.

2. Recalculate your "Net Price" expectations.

Don't look at the sticker price of the schools on your list. Look at the net price and subtract what you can actually afford plus the $20,000 federal cap. If the gap is still $30,000 per year, you need to find a way to cover that without federal parent loans.

To run this calculation automatically for any college on your list, try our free Affordability Estimator. No login required. Pick your income bracket or paste your federal SAI, and the tool shows your estimated net price plus your Parent PLUS gap under the new $20,000 cap, for any school in our database.

3. Audit your student's college list for "Financial Safeties."

In the old world, a safety was a school where your kid could get in. In the 2026 world, a safety is a school your kid can get into AND that you can afford under these new caps. You need at least two schools on the list where the total four-year gap is under $65,000.

4. Move your borrowing timeline up if you have a senior.

If your child is a senior, make sure your loan applications are processed and originated before July 1. This could be the difference between being grandfathered into the old system or being stuck with the new caps and losing a practical path to PSLF eligibility on new loans.

5. Research merit aid over brand names.

If you can't borrow the difference, you need the school to give you the difference. Focus on schools where your student's GPA and scores are in the top 25 percent. These schools are much more likely to offer merit scholarships that reduce the need for loans in the first place.

Why My School List is your financial co-pilot

When we started My School List, we did it because the college planning system was broken. It shouldn't cost $15,000 to get good advice. And it shouldn't take a law degree to figure out if you can afford to send your kid to their dream school.

We are currently building out even deeper affordability tools to help you navigate these new Parent PLUS caps. Our platform already helps you see your real admission odds for over 1,000 schools. This is critical because the best way to avoid a loan trap is to get into a school that actually wants your student and will pay for them to be there.

Our mission is equal access to guidance. Whether you are a first-generation family or a seasoned parent who has done this three times before, the rules just changed for everyone. You don't have to navigate this alone.

We are here to help you build a list that is academically exciting and financially responsible. If you want to stay ahead of these policy changes and find schools that fit your new budget reality, join us.

Ready to take the stress out of college planning?

Don't wait until the July 1st hammer drops to figure out your budget. Start building a smarter, safer college list today.

Sign up for a free trial of My School List here.

Get personalized odds, merit aid estimates, and the peace of mind that comes with a real plan. We just launched our free Affordability Estimator, built specifically for the OBBBA changes. Estimate your real cost at any school under the new $20,000 Parent PLUS cap before you sign up for the full platform.

Disclaimer: Financial aid policies, federal loan limits, and interest rates are subject to change by the Department of Education and legislative action. Always verify the latest terms at studentaid.gov.

Related posts

Scholarship Search for High School Seniors

Beyond the Big Names: Building a Realistic College List This Summer

How to Choose the Best College Financial Aid Offer (Compared)

The Decision Day Countdown: What Seniors are Learning About Merit Aid (and Why Juniors Should Listen)

Ready to build your college list?

Take our free College Fit Quiz at getmyschoollist.com/quiz

Take the Free Quiz →