April 27, 2026

How to Choose the Best College Financial Aid Offer (Compared)

By Peter Young, Founder of My School List

If your kitchen table looks like a financial paperwork explosion right now, you are not alone.

There's the award letter from one college, the portal screenshot from another, a sticky note with tuition numbers scribbled on it, and maybe a cold cup of coffee sitting beside all of it. For many families, this is the moment when college stops feeling theoretical and starts feeling very, very real.

And honestly, this part can be exhausting.

As a former educator and school leader with 23 years total in education, 8 years as a teacher and 15 years as a principal, I've spent a lot of time working with families through big school decisions. One thing I've learned is that college financial aid letters can make smart, thoughtful parents feel like they suddenly need a translator, an accountant, and a stress-management plan all at once.

That's because colleges don't make this easy. The letters aren't standardized. The language is inconsistent. And some of the biggest numbers on the page are the least helpful ones.

So let's slow it down and make this practical.

If you're trying to compare college financial aid offers, the goal is not to figure out which school gave the biggest-looking package. The goal is to figure out which offer is actually best for your family over four years, not just the first semester.

Start Here: Big Numbers Can Be Misleading

One of the most common mistakes families make is looking at the total "aid" number and assuming the college with the biggest number is the best deal.

But that number can be wildly misleading.

A college might say your student received $42,000 in "awards." That sounds amazing until you realize part of that total includes loans, work-study, or discounts that don't function the way parents assume. In other words, not every dollar listed on the page lowers your actual bill.

That's the first mindset shift I want you to make: not all aid is free money.

Some aid is wonderful. Some aid is helpful but limited. And some aid is simply debt dressed up in friendlier language.

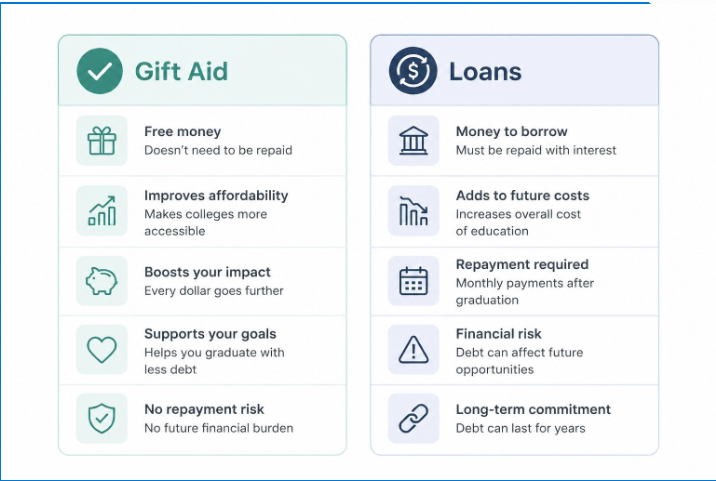

What Actually Counts as "Free Money"?

When families compare offers, I encourage them to separate each line item into plain-English buckets.

Grants and Scholarships

This is the category you want to love. Grants and scholarships reduce what you actually have to pay. They do not need to be repaid.

This includes federal grants, state grants, and institutional scholarships. It also includes merit-based scholarships, which are often tied to grades, test scores, course rigor, or other parts of a student's profile.

But here's the important nuance: not every "scholarship" is as generous as it sounds. Some colleges use scholarship language for what is essentially a broad tuition discount offered to many admitted students. That doesn't make it bad, but it does mean the label can sound more exclusive or more substantial than it really is. What matters is not the name. What matters is how much real cost it removes.

Work-Study

Work-study is not cash handed to your family upfront. It is an opportunity for your student to earn money through a campus job.

That can be valuable. It can help with books, transportation, or day-to-day expenses. But it should not be treated the same way as a grant. If a school includes $3,000 in work-study in the total package, that does not mean your bill is instantly $3,000 lower.

Loans

This is where many families get tripped up.

Federal Direct Loans are often listed right inside the "awards" section, right next to grants and scholarships. But they are not free money. They are debt.

Yes, federal student loans can be safer than many private loans. Yes, they may play a role in some families' plans. But they should never be confused with a scholarship just because they appear in the same column on an award letter.

If you remember one sentence from this article, let it be this: a loan may help you pay the bill now, but it does not reduce the price of college.

The Side-by-Side Comparison That Actually Helps

If you have multiple offers on the table, the best thing you can do is compare them in one clean format.

You do not need a fancy spreadsheet. You just need one place where each college is judged by the same categories.

Here's a simple comparison table you can use at your kitchen table:

| School Name | Sticker Price | Grants/Scholarships | Loans | Work-Study | Net Cost | Renewal Conditions |

|---|---|---|---|---|---|---|

| College A | $78,000 | $32,000 | $5,500 | $2,500 | $46,000 | Merit aid renewable with 3.5 GPA, full-time enrollment |

| College B | $54,000 | $18,000 | $5,500 | $2,000 | $36,000 | Scholarship renewable with 3.0 GPA |

| College C | $31,000 | $6,000 | $5,500 | $2,000 | $25,000 | Grant renewable annually after FAFSA review |

And here's the formula behind that table:

Net Cost = Sticker Price - Grants/Scholarships

Notice what is not subtracted in that formula: loans and work-study.

That's intentional.

Loans still have to be paid back. Work-study still has to be earned. If you subtract those too, the college can look cheaper on paper than it really is.

The Renewal Trap Families Miss

This is one of the biggest issues I see families overlook, especially when the first-year offer feels exciting.

A lot of merit-based scholarships are not guaranteed forever just because they appear in the freshman-year package. They often come with renewal conditions buried in small print, and those conditions matter more than most families realize.

A scholarship may require your student to maintain a 3.0 GPA. Some require a 3.25 or 3.5 GPA. Others require full-time enrollment, a certain number of credits completed each year, or continued progress in a specific major.

That might sound manageable in April of senior year. But freshman year of college is an adjustment. Students are managing harder academics, new independence, time management, and sometimes a difficult social transition all at once. It is not unusual for strong students to have a bumpier first year than expected.

And when that GPA slips below the renewal threshold, the scholarship can disappear.

That's the renewal trap.

A school that looks affordable in year one can become dramatically more expensive in year two. If a student loses a $15,000 merit scholarship after freshman year, that isn't a small change. That is a family budget crisis.

So before you fall in love with a number, ask these questions:

- Is this grant or scholarship guaranteed for four years?

- What GPA is required to keep it?

- Is that GPA cumulative or yearly?

- Does the student need to stay in a certain major?

- Does the award increase if tuition increases, or does it stay flat?

- Ask about typical renewal rates, even if exact numbers aren't published.

Those are not annoying questions. They are exactly the right questions.

What Parents Should Watch for in the Fine Print

Beyond renewal rules, there are a few other details that deserve a second look.

First, confirm the full sticker price. Some letters focus heavily on tuition but leave out room, board, fees, travel, and books in a way that makes the final number feel smaller than it really is.

Second, check whether the scholarship is institutional, federal, or state-based. Institutional aid may be tied more tightly to enrollment status or academic performance. Federal and state aid can also change depending on updated FAFSA information.

Third, watch for language that groups all funding together under a heading like "financial aid offer" or "total award." That wording can make the package sound more generous than it is if a chunk of it is simply borrowing capacity.

When in doubt, break every line into one of three labels:

- free money

- earned money

- borrowed money

That one exercise can clear up a surprising amount of confusion.

The Best Offer Is Not Always the Cheapest One Today

This is where families often need both math and perspective.

The best college financial aid offer is not always the one with the lowest first-year net cost. It's the one that fits your student, has realistic college admission odds, and remains financially sustainable.

That matters because the "cheapest" option can still be the wrong fit if transfer risk is high, if support is weak, or if your student is unlikely to thrive there. On the flip side, the "dream school" can become a painful burden if the package depends on shaky renewal terms or large annual borrowing.

This is why I encourage families to think in terms of fit, affordability, and likelihood all at once.

A personalized college list helps with that long before award letters arrive. When students build a college list around academic fit, budget, and real college admission odds, families are far less likely to end up surprised by April.

Why This Matters Earlier Than Senior Spring

If you're reading this as the parent of a 9th, 10th, or 11th grader, this is where you can save yourself a lot of future stress.

Too many families build a college list based mostly on names, rankings, and emotion, then only start thinking seriously about cost after acceptances roll in. By then, options feel personal, and the financial reality can hit hard.

A better path is to start earlier with better information.

At My School List, families can start with our free College Fit Quiz, no credit card required, or upload a transcript and get a personalized college list with real admission odds and projected merit aid ranges for 1,000+ schools. That means you can start identifying colleges where your student is not only a strong fit academically, but also more likely to receive meaningful merit-based scholarships.

That changes the conversation.

Instead of guessing, families can build a list around schools that are more realistic, more affordable, and more aligned with what their student actually wants.

A Simple Kitchen Table Checklist

If you're in comparison mode right now, here's a straightforward way to move forward tonight:

- Gather every award letter and portal printout in one place.

- Find the full sticker price for each school, including tuition, room, board, and fees.

- Add up only the grants and scholarships.

- List Federal Direct Loans separately so you can see the debt clearly.

- Put work-study in its own column.

- Calculate the real net cost.

- Read the renewal conditions for every grant and scholarship.

- Ask what the four-year picture looks like, not just freshman year.

If the numbers still feel muddy, call the financial aid office and ask them to walk you through the offer in plain English. Families do this every year. You are not bothering them.

Final Thought

If your kitchen table feels heavy right now, that makes sense. These decisions carry emotion, hope, and a lot of financial pressure.

But clarity helps.

When you separate free money from debt, pay attention to renewal rules, and compare every school the same way, the fog starts to lift. And when families start earlier with a personalized college list, real college admission odds, and realistic merit aid expectations, they make stronger decisions with far less panic.

That's exactly why we built My School List.

If you want a simpler way to plan, visit getmyschoollist.com. Take the free College Fit Quiz, no credit card required, or upload your student's transcript to get a personalized college list with real admission odds and merit aid ranges for 1,000+ schools.

Related posts

Scholarship Search for High School Seniors

Beyond the Big Names: Building a Realistic College List This Summer

Parent PLUS Loan Changes for 2026: What Families Need to Know

The Decision Day Countdown: What Seniors are Learning About Merit Aid (and Why Juniors Should Listen)

Ready to build your college list?

Take our free College Fit Quiz at getmyschoollist.com/quiz

Take the Free Quiz →